The FIRE movement (Financial Independence, Retire Early) has gained significant momentum in recent years, with many individuals striving to retire early by aggressively saving, investing, and living frugally. However, FIRE is not just about quitting work—it’s about achieving financial independence, where you have enough assets to live comfortably without relying on a traditional paycheck.

Of course, nothing comes without sacrifice, and FIRE is no exception. Achieving financial independence requires more than just cutting expenses—it demands time, discipline, and commitment. So, if you're considering joining the movement, what should you know? Let’s dive in.

At its core, FIRE is about achieving financial independence as quickly as possible so you can retire earlier than the traditional retirement age. The strategy involves:

To me, it’s the complete opposite of the "YOLO" mentality, where people prioritize spending now without worrying about the future. FIRE is about delayed gratification—making intentional financial choices today to gain freedom later.

To successfully reach FIRE, it focuses on two main areas: building wealth and reducing costs. Here’s how it's usually broken down:

The first step is determining how much money you need to retire early—this is called your FIRE number. A common rule of thumb is the 25x rule, which suggests saving 25 times your annual expenses.

This concept is borrowed loosely from the 4% Rule, which assumes you can withdraw 4% of your portfolio annually (adjusted for inflation) while maintaining financial stability.

To reach that FIRE number quickly, you’ll need to save a significant portion of your income—often 50% or more. These savings are typically invested in:

The key is to build wealth while keeping your living expenses low.

FIRE isn’t just about making more money—it’s about spending less. To reach financial independence faster it requires:

While FIRE is an attractive goal, it’s not without its drawbacks. Here are some key issues to consider:

Like mentioned, the FIRE number is an idea borrowed form the 4% Rule. However, the 4% Rule was developed based on historical data, assuming:

However, if you retire at 50 and live until 95, that’s a 45-year retirement—15 years beyond the rule’s original parameters. While the rule isn’t invalid, it may not be as reliable for ultra-long retirements. Some FIRE followers adjust their withdrawal rate to 3.5% or even 3% for added security, which means either needing more wealth parked on the side or a smaller draw from the portfolio.

The trade-off with FIRE is extreme discipline now for financial freedom later. This means:

Some people embrace this challenge, while others find it too restrictive. FIRE is a lifestyle commitment, and not everyone is comfortable with the sacrifices it requires.

Minimizing expenses is key in the early FIRE years, but it doesn’t stop once you retire. The less you withdraw from your portfolio, the longer your savings last. This means:

Some FIRE retirees return to work because they underestimated long-term costs. It is a new lifestyle overall.

One of the biggest challenges emerging from the FIRE movement is what comes next. Many people reach early retirement only to ask: Now what?

Some realize they don’t actually enjoy not working and want to return to the workforce. Others miss the structure and purpose that a career provides. Many want to work, but on their own terms—whether that means fewer hours, a passion project, or freelancing.

The problem? Many FIRE followers spend years optimizing their finances but little time planning what they’ll actually do post-FIRE. Some only realize this years later, leading to unexpected lifestyle adjustments. Because of this, some people in the FIRE community have altered their approach.

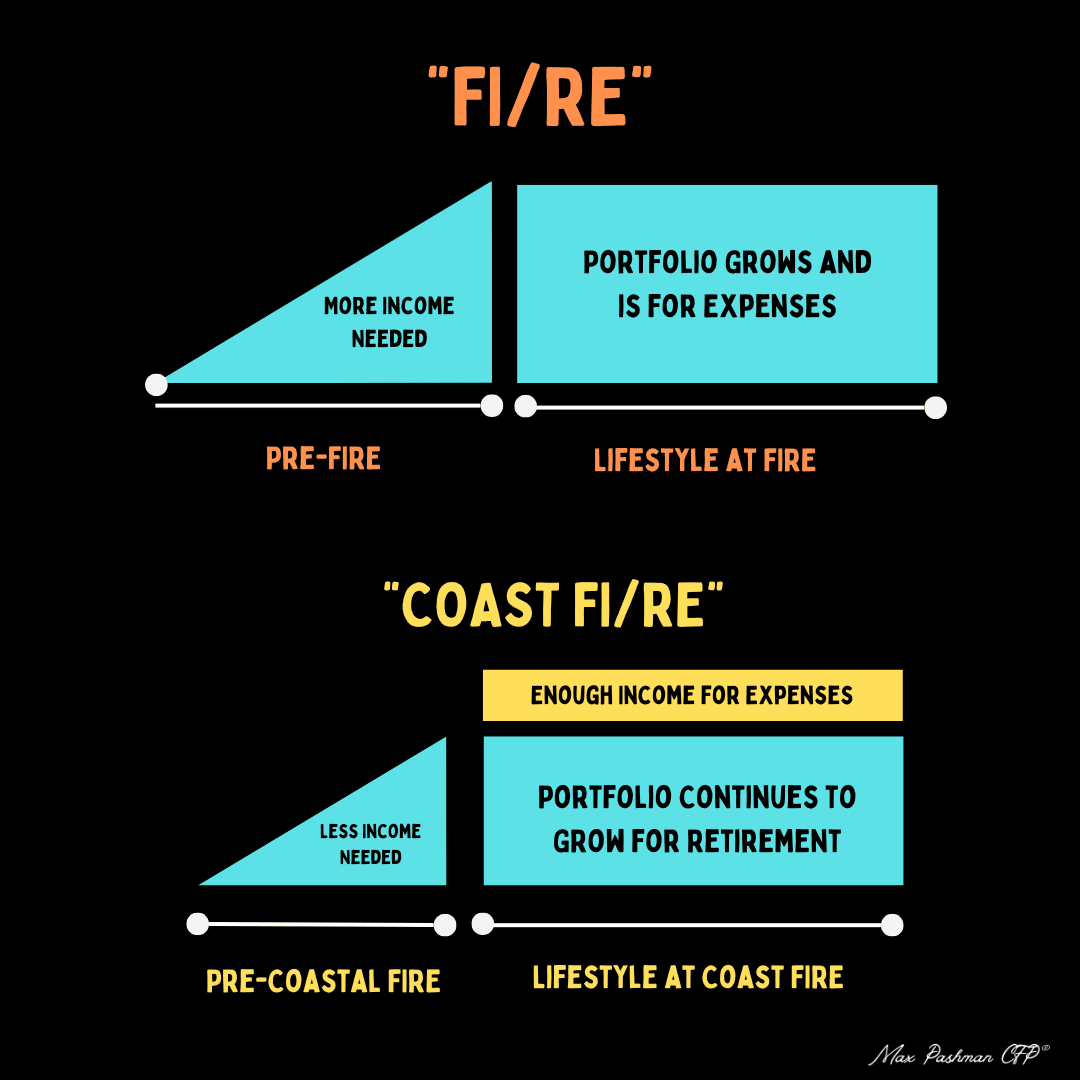

Recognizing the challenges of extreme FIRE, a new trend has emerged—Coast FIRE. This approach offers a middle ground, allowing individuals to achieve financial security without the intense sacrifices of traditional FIRE.

One variation of the FIRE movement is Coast FIRE, which offers a more flexible path to financial independence. Unlike traditional FIRE, which requires aggressively saving until you can retire early, Coasl FIRE is about reaching a point where your investments will grow on their own—eventually covering your living expenses by the time you reach traditional retirement age. This approach allows you to save aggressively in the early years and then ease up, without needing to contribute as much in the future.

The FIRE movement is about taking control of your financial future, but it requires serious commitment and sacrifice—balancing today’s lifestyle with tomorrow’s security. While full FIRE demands extreme savings and early retirement, Coast FIRE offers a more flexible alternative, allowing you to align your financial plan with your personal goals and career choices.

Most importantly, the FIRE community is a strong and supportive network with individuals on their own unique paths to financial freedom. Time to fire up those efforts!

Disclaimer: Pashman Financial LLC, its owners, officers, directors, employees, subsidiaries, service providers, content providers and third-party affiliates referred to as “Pashman Financial” do not offer the sale of securities or other investments. None of the information provided is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement, of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. The content is provided ‘as is’ and without warranties, either expressed or implied. Pashman Financial does not promise or guarantee any income or particular result from your use of the information contained herein. Under no circumstances will Pashman Financial LLC be liable for any loss or damage caused by your reliance on the information contained herein. It is your responsibility to evaluate any information, opinion, or other content contained. Please seek the advice of professionals regarding the evaluation of any specific content. Information on this email and website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized. The information on this site is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Pashman Financial LLC (referred to as “Pashman Financial”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose. Pashman Financial does not warrant that the information will be free from error. None of the information provided on this email and website is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall Pashman Financial be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the materials in this site, even if Pashman Financial or a Pashman Financial authorized representative has been advised of the possibility of such damages. In no event shall Pashman Financial LLC have any liability to you for damages, losses, and causes of action for accessing this site. Information on this email and website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.

You know how to make money, but you're not sure if you're making the right moves financially. That's why I started Pashman Financial.

.png)

PASHMAN FINANCIAL, LLC (“Pashman Financial”) is a registered investment advisor offering advisory services in California and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The presence of this website on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute. Follow-up or individualized responses to consumers in a particular state by Pashman Financial in the rendering of personalized investment advice for compensation shall not be made without our first complying with jurisdiction requirements or pursuant an applicable state exemption. All written content on this site is for information purposes only. Opinions expressed herein are solely those of Pashman Financial, unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to other parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.